The US dollar has been the dominant currency in the international market for approximately 80 years, surpassing the sterling pound and consolidating its position as the currency of reference after the World War II, with the Bretton Woods agreements and later the petrodollar[1]. By then, the United States had already surpassed the United Kingdom as the largest economic power (in fact, that happened in 1870), but it hadn’t been able to establish its currency as the dominant one until after the war, when Great Britain abandoned the gold standard[2] and began to pile up debt. Today, we find ourselves in a situation that could change this and dethrone the king of currencies.

Given the extreme tariff policies implemented by the current US President, Donald Trump, that caused a stir around the world, all countries were left searching for answers on how to protect themselves against such measures. This “crisis”, which was partially and quickly reversed by the US government through a 90-day pause, brought to light the international economic system’s dependence on the dollar; a dependence that was established when the government’s decisions were more predictable.

More than 90% of foreign exchange transactions involve the US dollar, and it accounts for approximately 55% of global reserves. Therefore, it’s easy to imagine how established its position is in the world and how difficult it would be to change it. However, there is more than one factor driving this change, one of them being tariffs. Importers generally don’t want to bear the cost of these tariffs, so they decide to pass them on to consumers and increase the price of the product.

The problem stems from President Trump’s decision to impose tariffs on the vast majority of products, causing inflationary pressures — which have yet to manifest. In turn, since the United States is such a huge importer — in fact, it imported the equivalent of $365 billion in 2024 — this wreaked havoc on international trade. More importantly, potential inflation, along with the difficulties of trading with them due to tariffs, would possibly lead to stagflation[3]. The increase in general prices would not be accompanied by greater profits for companies. Therefore, workers’ wages will not increase, which means lower real wages, which translates into less consumption and, ultimately, less economic growth.

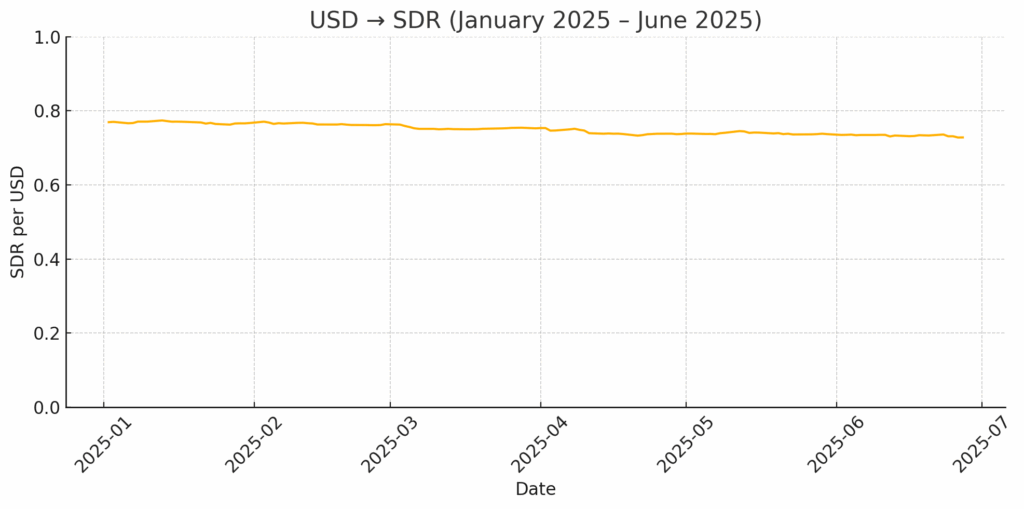

Normally, the implementation of such tariffs would lead to currency appreciation, as there would be fewer imports and therefore a smaller trade deficit, thereby providing further support for the currency. Furthermore, the Federal Reserve had raised interest rates with the same purpose[4]. However, despite all this, the currency depreciated. The only explanation for this is a loss of confidence in the Trump administration, its policies, and American institutions, fearing other possible erratic decisions he might make on the fly. The following chart shows the fall of the dollar against the Special Drawing Rights (SDR)[5]:

Source: International Monetary Fund.

Over the past six months, the dollar has depreciated by approximately 10% against the SDR, a near-unprecedented level.

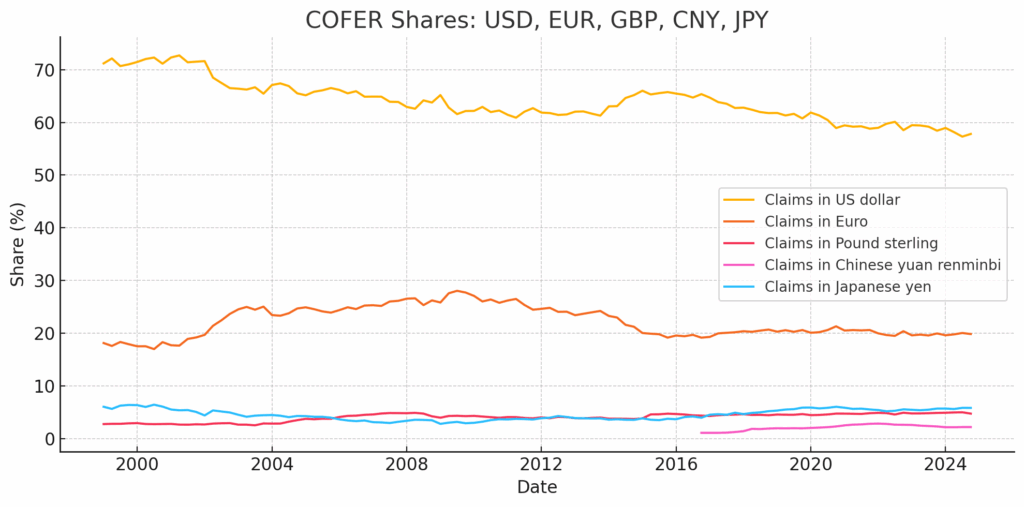

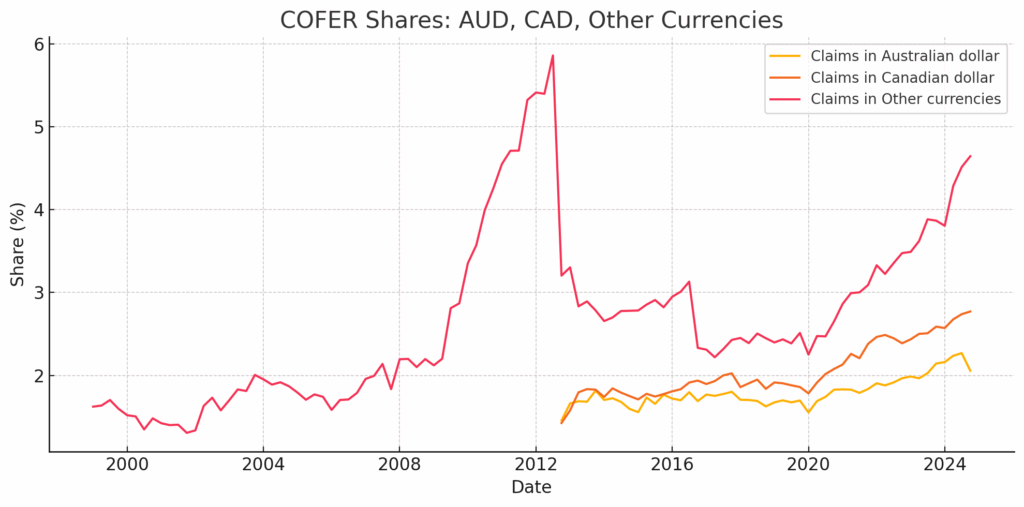

Additionally, the following graphs made with data from the International Monetary Fund (IMF) from 1995 to 2024 show the decline in the dollar’s reserves, while the use of other currencies increases:

Source: IMF.

Analyzing this data, we see a clear decline in the use of the dollar as a reserve, falling from over 70% to less than 60% of global reserves. This is still a very high level, but it does reflect the trend in currency use. At the same time, we see the rise of other less conventional currencies, such as the Canadian and Australian dollars. Lastly, almost 5% of global reserves are composed by other currencies.

It’s worth clarifying that the sudden increase and subsequent drop that occurred around 2012 is due to the currencies that were included in the “Other Currencies” category. Initially, “Other Currencies” included all currencies except the US dollar, the British pound, the euro, the Swiss franc, and the Japanese yen. Later, the Canadian and Australian dollars were also separated from the category (similarly, the same happened with the Chinese renminbi), like it can be seen in the chart.

Therefore, it could be said that the US dollar’s hegemony is lost and that it’s only a matter of time before another currency takes its place. The reality is that the conditions necessary for one or more currencies to become as big as the US dollar are complex, and the analysis is not so simple. Therefore, to study them, we will use the case of the sterling pound, which enjoyed a hegemony similar to that of the US dollar from 1871 until it was replaced by the US dollar itself.

First, the pound enjoyed its peak during the rise of the industrial revolution. The British were the largest exporters of industrial products and, in turn, the largest importers of raw materials, absorbing 30% of all imports from the rest of the world. This already tells an important condition: the country must have significant foreign trade, since trade is what gives the currency its use and keeps it circulating. Therefore, a country with an internationally dominant currency must have a high gross domestic product (GDP)[6]. However, this alone is not enough.

As explained above, by 1870 the American economy had already surpassed the British one. In fact, by 1900 the German economy had also surpassed the British one, therefore, GDP isn’t the only relevant factor. According to Barry Eichengreen, an American economist and professor at Berkeley, the pound markets were the most liquid and deep in the world due to the size of the global networks established by the British Empire with the rest of the world. That is, they could absorb large volumes of transactions without significantly affecting asset prices, thanks to their high liquidity and broad participant base. Furthermore, the Bank of England never seriously interfered with the freedom of pound holders. Therefore, another condition is that the currency’s issuing country must have free, liquid, and deep markets.

Similarly, an equally important factor — although not purely economic — is the country’s institutions. The dollar could have overtaken the pound much earlier, but it didn’t because it lacked a central bank (the US Federal Reserve was founded in 1913). The central bank largely determines the liquidity of a currency. Added to this was the lack of deep, liquid, reliable, and open financial markets.

It’s worth clarifying that institutions aren’t simply those that regulate the market or the country’s finances, but rather all those that make it function. Institutions that, for example, don’t allow a president to simply issue any policy through emergency decrees or violate the country’s own constitution. If a president is capable of doing that, then that country doesn’t have strong institutions and will instill distrust in investors, especially if the incumbent’s policies are erratic. Similarly, it’s reasonable to think that the Chinese renminbi isn’t a stronger currency because of China’s institutions; these don’t allow the free flow of large amounts of capital in or out of the country, they have managed exchange rate bands, and there is state intervention in many other aspects of the economy.

Comparing these conditions with the United States, they are no longer the world’s largest export-producing economy, China has taken that place. Although, they remain the largest importer and have the largest GDP. Furthermore, the United States has the deepest and most liquid market in the world and, before the tariffs, the freest.

The debate over the dollar’s hegemony is resurfacing due to the sudden imposition of tariffs, which transforms the market into one with greater state oversight and calls into question American institutions. Doing what Trump did — imposing such significant tariffs overnight — is unprecedented and shows the country as unpredictable and volatile. The two things investors hate most.

Finally, a very important factor that also calls into question the dollar’s position: the US debt. In the 1960s, French Finance Minister Valery Giscard d’Estaing called the dollar’s hegemony an exorbitant privilege; the ability to issue debt in its own currency allows the country to accumulate $34 trillion of it, greater than its GDP of $28 trillion. The question is: to what extent is this debt sustainable? And to what extent will investors continue to trust the country?

A debt of such magnitude naturally causes market distrust — which is reflected as an increase in country risk — disincentivizing the inflow of capital through private investment and thus reducing international demand for the currency, causing a depreciation. If the government were to achieve a surplus, or, more realistically, reduce the deficit, then this would demonstrate to investors an intention to address the situation. This would increase confidence, reduce country risk, and encourage investment.

Despite that, the Trump administration decided to do the opposite, through the Big Beautiful Bill, Trump makes his first-term tax reform permanent and increases defense spending, among other things. The Congressional Budget Office estimates a $2.8 trillion debt increase over the 2025-2034 period because of the Big Beautiful Bill.

Another factor that goes hand in hand with debt is the famous debt ceiling, which puts a limit on how much debt the United States can incur. The problem is that every time the government is close to reaching this limit, they raise it even further. For example, the Big Beautiful Bill will increase it by $5 trillion, leaving the limit at $40 trillion, 143% of the current GDP. It doesn’t help that recent administrations have operated with deficits. To be precise, the last year the United States had a fiscal surplus was 2000, corresponding to a fiscal deficit in the last four terms[7].

Therefore, it is reasonable to believe that in the next five years we will begin to see the beginnings of a multi-currency international monetary system, where no single currency reigns supreme. This would occur because of a sharper and more rapid decline in the US dollar, driven by central banks’ search for diversified reserves to avoid their country’s dependence on the policies of another. For the same reason, banks will try to hold similar percentages of reserves in each currency. These currencies will likely be the US dollar, the euro, the Japanese yen, the sterling pound, the Chinese renminbi, the Canadian dollar, and the Australian dollar, with a greater emphasis on the first five.

Another possible candidate is the Indian rupee, which could take on a larger role and become a reserve currency. India has the fastest-growing economy in the world, is among the top 20 exporters worldwide – growing rapidly – and among the top 10 importers worldwide – also growing rapidly.But on the other hand, India faces many obstacles when it comes to investing in the country. For example, there is a 20% tax on interest earnings from Indian debt, forcing investors to seek ways around it. Similarly, India has a set of restrictions, further discouraging private investment. These are two things that India must somehow change, since — previously explained — it is not enough just to have the highest GDP, high imports, or high exports; it’s also important to have a strong, free market. Finally, to add to all this, over the past 23 years, the Indian rupee has depreciated 30% against the SDR, which means that if it ever wants to become a reserve currency, it still has a very long way to go.

[1] The petrodollar is the system in which international oil transactions are quoted and settled exclusively in US dollars.

[2] The gold standard consisted of a fixed exchange rate between the pound and gold.

[3] Inflation with little or no economic growth.

[4] A higher interest rate (normally) leads to a higher demand for dollar-denominated assets, which leads to a higher demand for the currency and consequently to its appreciation.

[5] Special Drawing Rights are an international reserve of the International Monetary Fund, and their value is based on a basket of five currencies: the US dollar, the euro, the Japanese yen, the Chinese renminbi, and the sterling pound.

[6] A high GDP implies high production of goods and services, something that goes hand in hand with a country that exports and imports a lot.

[7] It should be noted that this period includes the 2008 financial crisis and the 2020 pandemic.